Have Co-Op Boards Lost the Power of Endless Delay?

Since Mayor Adams left office, the New York City legislature has been revisiting some ideas that he disfavored and are overturning his vetoes. One of them might make it easier to buy a home in New York City.

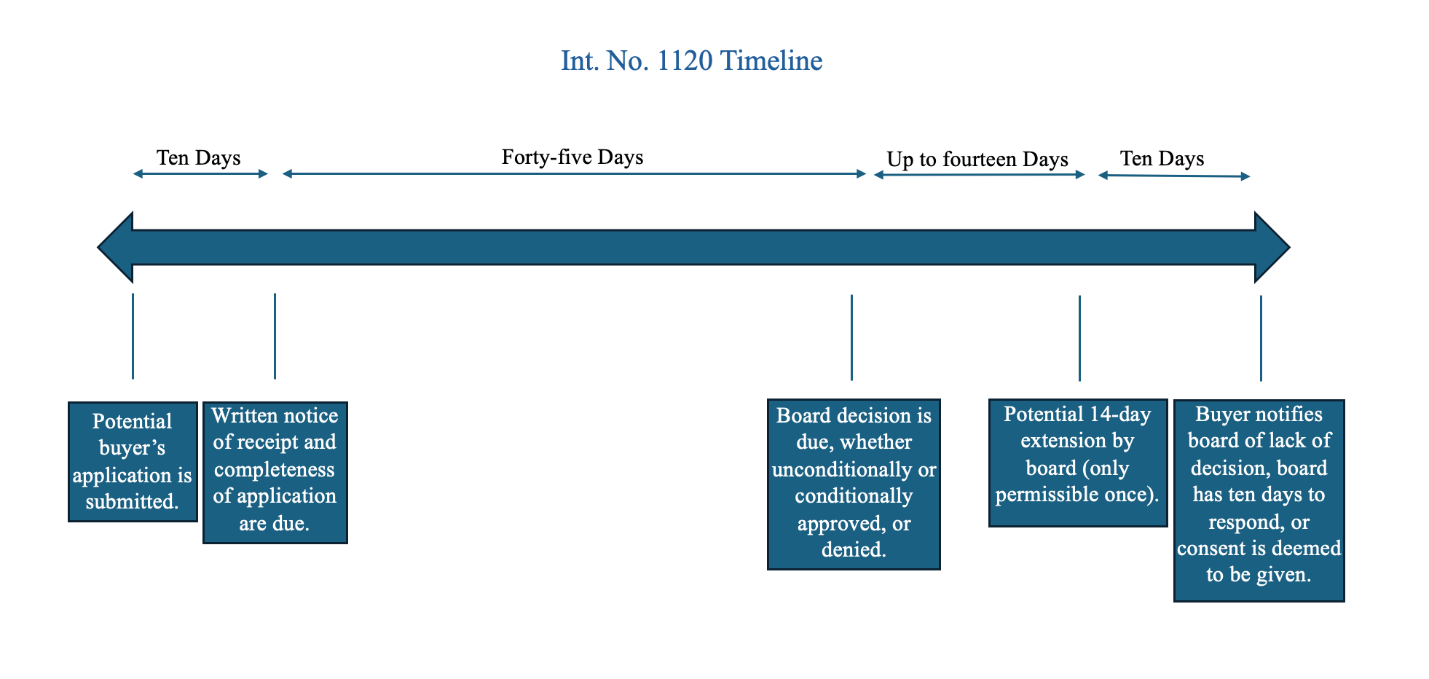

One of Adams’ vetoes that was recently overturned was targeting the bill “Int. No. 1120.” Known as Chapter 36, the Sale of Cooperative Apartments, it is an attempt to restrict the seemingly endless power of Co-Op boards to delay rendering a decision on a potential purchaser’s application.

Chapter 36 restricts co-op boards in multiple ways, but here is what you should know if you are buying or selling a unit in a cooperative:

- First, Chapter 36 does not apply to Co-Ops organized pursuant to the private housing finance laws in which their purchases are conditioned to approval by a state or city agency (sometimes known as “HDFCs”). It also does not apply to any Co-Ops containing less than 10 dwelling units.

- All Co-Op boards are required to have a standardized application process, with a list of required materials and fees associated with the application available to prospective purchasers and sellers.

- Once a prospective purchaser has submitted an application, the Co-Op board has fifteen days to provide written notice to the prospective purchaser both in email and, if possible, by registered mail. This notice must inform the prospective purchaser that the board received their materials and note any missing materials. This rule applies to both initial and subsequent applications.

- In the event that a Co-Op board fails to provide notice to prospective purchasers that their application is incomplete, the submitted application will be deemed to be complete.

- If the board does not meet in the months of July and August, and has a memorandum in place stating so, then the deadlines are tolled during this period.

- Once the board has received the complete application, it has up to 45 days to decide whether to approve, conditionally approve, or deny the application. The board may, one time, extend that 45-day period by 14 days without the consent of the prospective purchaser. The board may also request further extensions from the purchaser.

- If no decision is rendered after 45 days, and the Board has exercised their right to extend or requested an additional extension from the purchaser, the prospective purchaser may issue a written notice to the board noting their failure to provide a decision, and the board then has ten days to decide (that ten-day time frame must be communicated in the purchaser’s notice).

- If, after the ten-day period, the Board still has not rendered a decision, approval shall be assumed.

For those Co-Op boards that do not comply with the above deadlines, there are strict penalties. On the first instance that a Co-Op board fails to meet one of the prescribed timeframes, a $1,000.00 fine is imposed. The second time the board fail to meet the deadlines, the fine increases to $1,500.00, and for each subsequent failure the penalty increases to $2,000.00.

Below is a timeline flow chart showing how new law is anticipated to affect the coop application process.

For more information, or to speak with a licensed real estate attorney, reach out to info@whfirm.com or call us at 212-832-7400.

What Legally Counts as a Bedroom in New York City?

The information in this blog post was taken from the New York City Administrative Code and from the New York State Multiple Dwelling Law. You may refer to the relevant laws for more information. Our attorneys are not architects and would defer to architects regarding architectural matters.

In New York City, it’s not always obvious whether a room is legally considered a bedroom. Sellers, brokers, and even unit owners may mislabel rooms — either by accident or intentionally — to inflate an apartment’s value. If you are buying, renting, or renovating a unit, knowing the real rules can save you from serious legal and financial trouble.

Here’s what you need to know:

1. A Bedroom Must Be a “Habitable Room”

Under NYC law, only “habitable rooms” can qualify as bedrooms. A habitable room is a residential space where the ordinary functions of life occur — bedrooms, living rooms, kitchens, studies, and similar spaces. Hallways, closets, stairways, bathrooms, and laundry rooms are not habitable rooms.[1]

2. Minimum Size Requirements

A bedroom must meet strict minimum size standards:[2]

- At least 80 square feet of clear floor area.

- At least 8 feet in any horizontal dimension.

- A clear ceiling height of 8 feet for the minimum required area.

Note that some exceptions apply:

- In apartments with three or more bedrooms, up to half the bedrooms can have a minimum width of 7 feet.[3]

- A slightly smaller room (minimum 70 square feet) is permitted if it opens into an adjoining room by at least 60 square feet and meets lighting and ventilation standards.[4]

Takeaway: Buyers viewing units with small “bonus rooms” should measure carefully. Rooms that are too small cannot legally be considered bedrooms — which affects value and usability.

3. Window and Ventilation Requirements

Every legal bedroom must have proper light and air:[5]

- A window opening onto a street, yard, or court on the same lot.

- Window area must be at least 10% of the floor area.

- The openable portion must be at least 5% of the floor area.

- Minimum window opening size: 12 square feet.

Important: No window = no bedroom, legally. This is especially critical when assessing interior rooms marketed as “bedrooms.”

4. Privacy Rules: Bedrooms Must Be Accessible Without Passing Through Another Bedroom

In apartments with three or more rooms, bedrooms must have direct access:

- You must be able to enter a bedroom without walking through another bedroom.[6]

In converted buildings, access to at least one bathroom from any bedroom must be possible without passing through another bedroom.[7]

This protects privacy and is often a challenge in older “railroad” apartment layouts.

5. Bathroom Requirements Within Apartments

Another often-overlooked requirement is that the law mandates that apartments have their own bathroom facilities:

- Every apartment must have a private water-closet compartment (a room containing a toilet), separate from other apartments.

- In many cases, a separate bathroom or bathtub must also be provided.

- These facilities must be properly connected to water supply and drainage systems, and must be accessible from within the apartment.[8]

Takeaway: A bedroom must not only meet its own requirements, but the apartment it belongs to must also meet bathroom standards — otherwise, it could limit future resale, rental, or renovation plans.

6. No Closet Requirement

There is no legal requirement that a bedroom have a closet.

Buyers focused on storage should carefully review the layout — particularly in prewar or loft-style apartments where built-ins are rare.

7. Studios and Living Rooms: Bigger Minimums Apply

Where a living room doubles as a sleeping space — as in studios — it must be larger; at least 132 square feet for the primary living room in a Class A apartment.[9]

This prevents landlords or sellers from marketing extremely tiny spaces as full studios.

Why Bedroom Compliance Matters

- Apartment Valuation:

The legal bedroom count has a direct effect on an apartment’s market value. Overstating the number of legal bedrooms can artificially inflate asking prices and lead to problems during mortgage appraisals or resale. - Renovation Potential:

Owners seeking to install additional bedrooms must comply fully with minimum size, window, ventilation, and access requirements. Otherwise, new rooms may be deemed illegal, reducing the apartment’s value or creating liability risks. - Resale and Re-rental Risk:

If you later resell or rent your unit, marketing a non-compliant room as a bedroom can trigger lawsuits, fines, or rescinded sales. - Compliance Costs:

Bringing an apartment into compliance — for example, enlarging a too-small room or creating proper egress windows — can be costly. Building alterations often require Department of Buildings (DOB) permits and inspections, especially in landmarked properties.

Conclusion: Bedroom Basics for Buyers and Owners

When buying, renting, or renovating in New York City, it’s critical to verify that each bedroom meets the legal definitions — and that the apartment as a whole has compliant bathroom facilities. A bedroom is not just a matter of size — it’s a bundle of legal requirements covering dimensions, windows, privacy, and plumbing.

If you have any questions about whether a space qualifies legally, or if you’re considering renovations to maximize your apartment’s value, consult with a qualified real estate attorney or architect before making a decision.

Sources Cited:

[1] NYC Admin. Code § 27-232 (Definition of “Habitable Room”).

[2] Id. § 27-751; NY CLS Multiple Dwelling Law § 31(2)(b)-(d).

[3] Id.; NYC Admin. Code § 27-751(c).

[4] Id. § 27-751(a).

[5] Id. §§ 27-2058 et seq.

[6] NY CLS Multiple Dwelling Law § 82.

[7] Id. § 179.

[8] Id. § 76.

[9] NY CLS Multiple Dwelling Law § 31(2)(a).

What Sellers and Their Lawyers Need to Know About New York’s Fair Chance for Housing Act

As of January 1, 2025, New York’s Fair Chance for Housing Act (FCHA) is in effect, significantly limiting how criminal history can be considered when selling or renting housing. Sellers, brokers, development boards, and their representatives need to be aware of the following implications.

What Does the Law Do?

The FCHA prohibits discrimination based on an applicant’s criminal record when selling or renting a home. Sellers and landlords cannot reject an applicant or offer them different terms due to their past convictions—unless the record falls under the law’s strict “reviewable criminal history” guidelines.

What Criminal Records Can Be Considered?

Housing providers can only consider the following:

- Convictions on a sex offender registry regardless of when they occurred.

- Felony convictions from the past five years from the date of release from prison, or from the date of sentencing if no prison sentence was imposed.

- Misdemeanor convictions from the past three years from the date of release from prison, or from date of sentencing if no prison sentence was imposed.

However, sellers cannot consider:

- Arrests that did not lead to a conviction.

- Cases dismissed or resolved in favor of the defendant.

- Certain out-of-state convictions that conflict with New York law.

Background Checks: Strict Rules Apply

A background check cannot be conducted until after a conditional offer is made. A seller may not even make statements or questions relating to a purchaser’s potential criminal history until after a contract or conditional offer is signed. If the seller wishes to review an applicant’s criminal history after a conditional offer is made, they must:

- Provide written notice to the applicant about their rights.

- Promise in writing that the offer will not be revoked unless the criminal record falls within the FCHA’s “reviewable” category. If a decision is made against the applicant due to their criminal record, the seller must:

1. Conduct an individualized assessment of the applicant’s situation.

2. Provide a written explanation detailing how the criminal record directly impacts a legitimate business interest in the sale.

3. Give the applicant five business days to correct errors or provide additional information that would strengthen their application.

What Sort of Convictions May Housing Providers Rely on When Denying an Application for Housing?

If a seller wishes to deny an application based on the applicant’s reviewable history, they must identify an objective, specific, and non-discriminatory business interest, and explain the connection between the applicant’s reviewable criminal history and the stated business interest. The existence of a conviction alone never creates that link. Seller preferences or the preferences of existing tenants are also not permissible bases for a legitimate business interest. If the provider fails to provide relevant and credible evidence that directly relates to its proffered business interest, that interest will be considered speculative, and therefore not legitimate, and cannot be relied on to deny housing to an applicant.

What If You Violate the Law?

Failure to follow the FCHA’s process could lead to discrimination claims and legal liability. Even if a third-party background check provider is used, the seller is responsible for ensuring compliance. Applicants may file a complaint with the NYC Commission on Human Rights within one year of their application being denied. Violations may incur civil penalties of up to $125,000 per violation, or double for willful, wanton, or malicious violations. The Commission may also impose training and compliance programs on managers and employees.

Are There Any Exceptions?

Yes. The law does not apply if you are selling or renting part of your personal residence. Additionally, background checks are allowed when federal, state, or local laws require them, though sellers must still follow the FCHA’s notice and review procedures.

Can Sellers Deny an Application for Reasons Unrelated to Criminal History?

Yes, sellers and boards may still deny a housing application for reasons not related to criminal history without engaging in the Fair Chance Housing process. Thus, for example, an application may be denied for failure to meet standard contract conditions, such as mortgage contingencies and credit requirements, without requiring a review and correction process. Additionally, sellers may consider the violent history of an applicant or resident if such acts would adversely affect the health, safety, or welfare of other residents.

Bottom Line

If you are selling an apartment, you must follow strict procedures before considering an applicant’s criminal history. Sellers and their legal representatives should ensure full compliance with the FCHA to avoid potential legal consequences.

Welcoming our Newest Partners

Weidenbaum & Harari LLP is excited to announce the promotion of two of our attorneys, Jeffrey Baron and Eugene Sarantis, to partner!

Jeffrey has been practicing law for over fifteen years, with a focus representing purchasers and sellers of cooperatives, condominiums, and 1-4 family homes. Prior to joining Weidenbaum & Harari LLP, Jeffrey was a senior associate at a law firm specializing in real estate and banking transactions, and he is well versed in the nuances of residential financing, CEMAs, and refinances, in addition to his years of experience in the residential purchase and sale arena.

Eugene advises purchasers, sellers, owners, investors, developers, and lenders on a broad array of sophisticated residential and commercial real estate matters, including purchases, sales, leasing, financing, and access agreements. Eugene’s residential transactions include cooperative, condominium, single family, and multifamily purchases and sales, having closed notable transactions in NYC and the Hamptons. Eugene is familiar with all facets of cooperative and condominium ownership. Eugene’s commercial transactions include single asset and portfolio acquisitions and sales, joint ventures, and financing transactions related to all types of commercial properties. In addition, Eugene regularly prepares and negotiates retail, office, and industrial leases for landlords, tenants, and corporate clients in connection with commercial leasing transactions.

We are very pleased to have Jeffrey and Eugene joining us as partners!

Understanding the 467-a Tax Abatement – A Guide

The following information is reflective of the date that it was published, and does not constitute legal advice. Any questions about such matters should be directed to an attorney in order to discuss their specific circumstances

The 467-a New York City Cooperative/Condominium Tax Abatement allows individuals whose primary residence is a cooperative or condominium unit in New York City to realize savings on their annual property taxes. The cooperative/condominium board, or its managing agent, is responsible for applying for the abatement with the New York Department of Finance on behalf of all qualifying units within the building. Any unit owner who wishes to receive the abatement should inform their development that the unit is their primary residence, so that the development includes the unit owner in the development’s application. The Coop/Condo Tax Abatement was first instituted in 1996 and has been extended eight times. It is currently effective until June 30, 2026.

To qualify for the abatement, a unit owner must meet the following requirements:

- The unit owner must be an individual, not an LLC or corporation.

- A trust may qualify if all beneficiaries of the trust use the unit as their primary residence.

- The sponsor, and its successors in interest, may not qualify.

- The unit owner cannot own more than three units in the development, one of which must be their primary residence.

- The unit must be in Tax Class 2.

- Real Property Transfer Tax forms—or a Deed—must be filed with ACRIS on or before January 5 of the year in which an abatement on that unit is sought. Individuals who miss the deadline may file for the abatement by January 5 of the following year to begin receiving the abatement in that year.

- The unit owner must inform the development by February 15 of the year in which an abatement is sought that the unit is their primary residence.

- Individuals receiving a clergy property tax exemption do not qualify for the abatement.

The development must meet the following additional requirements for units within the building to receive the abatement:

- The development must apply for or renew the abatement by February 15 (or the following business day, if that date is a weekend or holiday).

- A prevailing wage affidavit must be filed for most developments, indicating that the building pays its workers in accordance with NYC Prevailing Wage laws.

- Certain buildings will not qualify for the 467-a Coop/Condo Tax Abatement:

- Buildings receiving the J-51, 420-c, 421-a, 421-b, and 421-g abatements cannot benefit from the 467-a Coop/Condo Tax Abatement.

- Buildings associated with the following also cannot receive the Coop/Condo Tax Abatement:

- Housing development fund corporations (HDFC).

- Limited dividend housing companies.

- Redevelopment companies.

- Mitchell-Lama buildings.

- Division of Alternative Management Programs (DAMP).

- Urban Development Action Area Program (UDAAP).

Unit owners may realize an abatement to their property tax bill based on the assessed value of their unit. The following chart displays abatement percentages:

| Average Assessed Value | Abatement Percentage |

| $50,000 or less | 28.1% |

| $50,001 to $55,000 | 25.2% |

| $55,001 to $60,000 | 22.5% |

| $60,001 or more | 17.5% |

Attorneys, brokers, and their clients can coordinate their corresponding rights and obligations under the abatement rule by including provisions in the real estate contract to address pending or shared abatements, as well as abatements that are denied due to the fault of the seller or development. Purchasers should inquire whether a building qualifies for the abatement, and additionally whether the previous owner of their prospective unit was receiving the abatement. New owners should also be sure to promptly inform their development that their unit is being used as their primary residence. Failing to inform the development by the February 15 deadline will disqualify an owner from receiving the abatement.

Source:

N.Y. Real. Prop. Tax Law § 467-a (McKinney 2023).

What to Expect at the Closing Table: Cooperative Sales

Congratulations! You are almost to the finish line of your Co-op sale. Please take a moment to review the information below so that you may better understand what to expect as we approach your closing day. Some of the specifics described below may change based on the particular circumstances of your transaction. Please let us know if you have any questions or concerns regarding this information so that we may discuss them further with you.

1. Preparing to Close:

You should have already provided us with your most recent mortgage and/or HELOC statement(s). If IT-2664 non-resident tax forms and/or FIRTPA withholding apply to this sale, please ensure that these items were discussed with your attorney prior to scheduling the closing date.

If you do not wish to attend the closing in person, you may assign our firm to be your agent via power of attorney. If this has not already been discussed, please be sure to let us know as soon as possible if this is something you are interested in. If you are located overseas or in a location where there will be delays in the preparation and execution of power of attorney documents, this option may not be possible.

Once a closing date is set, please check with us before making any maintenance payments and please turn off any applicable automatic bill payments.

2. Closing Statement:

The closing statement includes a breakdown of closing expenses and payments, stating how they will be paid and from where. All of the fees due for your sale, including any applicable mortgage (and payoff attorney/UCC3 termination fees), any broker commissions, NYC/NYS transfer taxes (along with preparation and filing fees), any unpaid maintenance, co-op/management/transfer agent fees, and any fees due to our firm will all be accounted for, along with the estimated balance due to you as Seller. You will generally receive the draft closing statement between 1-3 days prior to the closing. However, there are certain circumstances where the receipt of the closing statement may be delayed further.

• Once received, please review the closing statement, and let us know if you have any questions.

• Typically, bank checks are provided for in-person closings, though sometimes wires may be necessary and/or accommodated. Please note that official bank checks and attorney escrow checks often take one week or more to clear. You should contact your bank for details on clearance times if you have any questions or concerns.

• If a move-out deposit is collected at closing, it is best practice to pay it via personal check. This allows for the deposit funds to be voided or otherwise refunded more efficiently.

• If you have assigned our firm to close for you via power of attorney, we will advise you on the available options to send the balance funds to you.

3. Walkthrough:

The Purchaser will typically coordinate a final walkthrough with their broker. Utilities should not be turned off until after closing in order to allow the Purchaser to check that everything is working.

The standard practice in New York is to perform the final walkthrough the day before the closing (and sometimes even the morning of the closing). Issues discovered during the walkthrough may be troublesome due to limited time to correct them (assuming the Contract states that the Seller is required to make any repairs).

• Please be sure to keep an eye out for emails and/or calls from your broker and our firm ahead of the closing.

• If there are walkthrough issues that remain unresolved prior to closing, we can discuss a way forward, as there are some options that may still allow you to close but with a credit, escrow, or other solution.

• If you are not attending the closing, and have made prior arrangements for our office or someone else to close with appropriate power of attorney forms, please be sure to be available via phone so that we can discuss options if needed.

4. At the Closing Table:

Be sure to bring a valid photo ID to the closing, such as an unexpired driver’s license or passport. You should also bring along any available keys for the unit, building and mailbox (as applicable).

We generally advise clients to allot about 2 hours for the closing, though some closings can take longer if there are issues for the parties to resolve, bank-related delays, parties running late, etc. At the closing you can expect to see the Transfer Agent (the individual acting on behalf of the Co-op), the Purchaser’s Attorney, the Purchaser, the Bank Attorney (where applicable), and an attorney from our office appearing on your behalf. In addition, if you have a mortgage, a representative from that bank will be stopping by the closing to pick up the mortgage payoff check (which we will have the Purchaser bring on your behalf) and drop off the original Stock and Lease for the Transfer Agent to cancel once the closing is completed.

Once you get settled in at the table, a series of documents will be exchanged between and among the parties. We will explain to you the documents that you need to sign and their significance in the transaction. If you have any questions, you will have an opportunity to ask us at that time.

Examples of documents you may encounter at the closing:

• Bank documents. If the Purchaser is getting a loan, there will be lender documents for you to sign. It is important to sign these documents first because the bank documents will likely need to be sent to the bank’s closing department for funding approval, which can take some time.

• City/State transfer documents. These documents are commonly referred to as ACRIS documents. These documents let the State/City know who is involved in this transaction and the amount of tax to be paid on the deal, and by whom. Unless otherwise noted, the Seller is the responsible party for the NYS and NYC transfer taxes. If the Purchase Price is one million or greater then there is a Purchaser imposed tax as well.

• Co-op documents. The Transfer Agent will need signatures on documents required by the Co-op to facilitate the transfer.

Once the required documents have been signed, any walkthrough issues have been resolved, and the lender has funding approval (if your buyer has a loan), the Transfer Agent will confirm with the Purchaser and Seller that we are clear to close.

The Transfer Agent will make copies of all documents exchanged for the Seller/Buyer/Bank. The keys will be released to the Purchaser and the checks released to the Seller. If you have a mortgage, then the payoff contact will deliver the payoff to your lender.

Congratulations! By this point, you have made it to the finish line and are now closed. After the closing, we will send you the final closing statement, which you can provide to your accountant during tax time.

If you have any questions about the above summary, please let us know – we want to make the process as smooth and seamless as possible for you.

What to Expect at the Closing Table: Condominium Sales

Congratulations! You are almost at the finish line of your Condominium sale. Please take a moment to review the information below so that you may better understand what to expect as we approach your closing day. Please note that some of the specifics described below may change based on the particular circumstances of your transaction. Please let us know if you have any questions or concerns regarding this information so that we may discuss them further with you.

1. Preparing to Close:

You should have already provided us with your most recent mortgage and/or HELOC statement(s). If IT-2663 non-resident tax forms and/or FIRTPA withholding apply to this sale, please ensure that these items were discussed prior to scheduling the closing date.

If you do not wish to attend the closing in person, you may assign our firm to be your agent via power of attorney. If this has not already been discussed, please be sure to let us know as soon as possible if this is something that you are interested in. If you are located overseas or in a location where there will be delays in the preparation and execution of power of attorney documents, this option may not be possible.

Once a closing date is set, please check with us before making any common charge or tax payments, and please turn off any applicable automatic bill payments.

2. Closing Statement:

The closing statement includes a breakdown of closing expenses and payments, stating how they will be paid and from where. All of the fees due for your sale, including any applicable mortgage, any broker commissions, NYC/NYS transfer taxes (along with preparation fees), any unpaid property taxes or common charges, condo/management fees, and any fees due to our firm will all be accounted for, along with the estimated balance due to you as Seller. You will generally receive the draft closing statement between 1-3 days prior to the closing. However, there are certain circumstances where the receipt of the closing statement may be delayed further.

• Once received, please review the closing statement, and let us know if you have any questions.

• Typically, bank checks are provided for in-person closings, though sometimes wires may be necessary and/or accommodated. Please note that official bank checks and attorney escrow checks often take one week or more to clear. You should contact your bank for details on clearance times if you have any questions or concerns.

• If a move-out deposit is collected at closing, it is best practice to pay it via personal check. This allows for the deposit funds to be voided or otherwise refunded more efficiently.

• If you have assigned our firm to close for you via power of attorney, we will advise you on the available options to send the balance funds to you.

3. Walkthrough:

The Purchaser will typically coordinate a final walkthrough with their broker. Utilities should not be turned off until after closing in order to allow the Purchaser to check that everything is working.

The standard practice in New York is to perform the final walkthrough the day before the closing (and sometimes even the morning of the closing). Issues discovered during the walkthrough may be troublesome due to limited time to correct them (assuming the Contract states that the Seller is required to make any repairs).

• Please be sure to keep an eye out for emails and/or calls from your broker and our firm ahead of the closing.

• If there are walkthrough issues that remain unresolved prior to closing, we can discuss a way forward, as there are some options that may still allow you to close but with a credit, escrow, or other solution.

• If you are not attending the closing, please be sure to be available via phone so that we can discuss options if needed.

4. At the Closing Table:

Be sure to bring along a valid photo ID for the closing, such as an unexpired license or passport. You should also bring along any available keys for the Unit, building and mailbox (as applicable).

We generally advise clients to allot about 2 hours for the closing, though some closings can take longer if there are matters for the parties to resolve, such as bank-related issues, parties running late, etc. At the closing you can expect to see the Title Company, the Purchaser’s Attorney, the Purchaser, the Bank Attorney (where applicable), and an attorney from our office appearing on your behalf. If you have a mortgage, the Title Company’s closer will typically pick up the mortgage payoff check (which we will have the Purchaser bring on your behalf) and file the Deed with the county. Note that the Condominium (or their management company) typically does not send a representative to the closing, and will usually provide their documents and schedule of fees owed prior to the Closing date.

Once you get settled in at the table, a series of documents will be exchanged between and among the parties. We will explain to you the documents that you need to sign and their significance in the transaction. If you have any questions, you will have an opportunity to ask us at that time.

Examples of documents you may encounter at the closing:

• Bank documents. If the Purchaser is getting a loan, there will be lender documents for you to sign. It is important to sign these documents first because the bank documents will likely need to be sent to the bank’s closing department for funding approval, which can take some time.

• City/State transfer documents. These documents are commonly referred to as ACRIS documents. These documents let the State/City know who is involved in this transaction and the amount of tax to be paid on the deal, and by whom. Unless otherwise noted, the Seller is the responsible party for the NYS and NYC transfer taxes. If the Purchase Price is one million or greater then there is a Purchaser imposed tax as well.

• Condominium documents. As mentioned above, the Condominium typically does not send a representative to the closing (though in some rare cases they will). Either way, the Condominium may have some standard documents to sign. They will often expect you to provide a forwarding address and contact details in case they need to reach out post-closing.

• Title documents. The title company may require you to sign a document acknowledging the title charges, paperwork related to your mortgage payoff (if any), as well as an affidavit acknowledging that you are not hiding any pertinent information not otherwise disclosed.

Once the required documents have been signed, any walkthrough issues have been resolved, and the lender has funding approval (if your buyer has a loan), the Title Company representative will confirm with the Purchaser and Seller that we are clear to close.

The Title Company Representative will make copies of all documents exchanged for the Seller/Buyer/Bank. The keys will be released to the Purchaser and the checks released to the Seller. The Title Company Representative will also take the Deed and file it with the appropriate authority. If you have a mortgage, then the Title Company will deliver the payoff to your lender.

Congratulations! By this point, you have made it to the finish line and are now closed. After the closing, we will send you the final closing statement, which you can provide to your accountant during tax time.

If you have any questions about the above summary, please let us know – we want to make the process as smooth and seamless as possible for you.

WHFirm Makes The Real Deal’s Top 40!

The Real Deal has published its annual list of NYC’s top real estate law firms, and Weidenbaum & Harari, LLP is pleased to once again make the cut!

TRD bases their ranking on the total dollar volume of closed sales recorded between the beginning of August 2023 and the end of July 2024, and factors in transactions in Manhattan, Brooklyn, and Queens.

While its always an honor to be recognized, our firm’s philosophy has always been to prioritize the client experience rather than the numbers. If you are planning a residential purchase or sale in NYC this year, we’d love to assist!

Tips from a New York Real Estate Attorney: When Should I Lock My Rate?

On the issue of rate locks, in our conservative opinion, it is a business decision as to precisely when to lock. Many clients wait to lock in a rate until they have been approved by the board, or at least after an interview has been scheduled. Since, unfortunately, there are many uncertainties, including that we do not know when the board interview will take place, much less when the board will render its decision, or when the seller will definitely seek to close, it may not be wise to lock-in a mortgage rate right away. However, this is a calculated business decision on the part of the buyer, based on a number of factors, including: the costs of locking a low rate early, the risk of not closing in the lock period, and the risk that rates may rise or fall in the future.

Please note that once a buyer decides to lock in their rate, if the closing takes place beyond the rate-lock period, they may have to pay substantial fees to the bank in order to maintain a loan through the closing date. Some banks do not even provide extensions past a certain point – each bank has different requirements and costs. The decision of when to lock in is obviously a personal one. However, we caution that the closing is not “set in stone” until after the buyer has been approved by the board, and even at that point, the sellers have the right to push the closing date back under a number of circumstances.

Please contact our office if you have any rate lock related questions, or wish to discuss your personal circumstances further.

Tips from a New York Real Estate Bank Attorney: Best Practices to Improve Saleability and Avoid Post-Closing Stress

Given the recent .50 basis point reduction in interest rates, mortgage applications are up substantially. Therefore, as the volume of closings increases, it is even more important to make sure that each individual closing is as smooth as possible. Everyone appreciates the feeling of a well-run closing.

NYC closings generally take up to two hours to close when there is financing. During that time, buyers, sellers, their attorneys, transfer agents, and real estate brokers spend some amount of time eyeing the bank attorney, and a collective mental push builds, urging the bank attorney to work faster, faster, faster.

However, a bank attorney’s job is really two-fold: The first is to make sure closing documents are quickly processed, approved, and funded at the closing table. The second is to ensure those documents are accurate, consistent, and complete, so there are no future issues when refinancing or transferring the loan after closing. The saleability of a loan is key for many lenders, so bank attorneys must balance these two jobs while keeping everyone happy.

The full loan package should be returned all at once with no lingering documents to follow. The items below are common requirements that should be double-checked at closing so that it is possible to submit a clean, complete loan package that helps your bankers and clients avoid common future pitfalls.

1. The Basics:

• Spelling of names, property addresses, loan amounts, signatures, and initialing the appropriate locations.

i. Be extra careful with the 1003 loan application, as signature sections can blend into the rest of the form.

ii. Some documents may require initials on every page (double check mortgages, rate lock agreements, notes).

• Any handwritten changes, if allowed, should be initialed in the margin.

2. For Cooperative Units:

• Triple check that all documents contain the correct number of shares.

• If the new stock certificate number is written in, have the borrower(s) initial this change.

• Include a copy of the recorded UCC1 in the closing package; the UCC1 should be recorded prior to closing.

• If a new proprietary lease is not issued for the borrower, each assignment of the original proprietary lease should itself be an original. Copies along the chain of leases/title may not be acceptable.

• Recognition Agreements should include the board members’ names typed or handwritten with their title under the signature line. Double check that the loan amount matches on the first page, as loan amounts often change after recognition agreements are provided to the board.

• Best Practice: If any cooperative or bank documents were signed by Power of Attorney, try to obtain an original power of attorney for the closing package. Without an original power of attorney in the closing package, documents containing power of attorney language will need to be regenerated without them when the loan is later transferred or sold.

3. For Houses or Condominiums: Stamp the mortgage as the “Certified True Copy” – this notation should not be handwritten.

4. CEMA Transactions: For a Consolidation, Extension, and Modification Agreement (“CEMA”), checking for typos and errors is additionally important.

• The Exhibit A (List of Mortgages and Assignments) should follow the mortgage schedule exactly. There should be no missing assignments, either previously recorded or to be recorded. Any assignments being recorded “simultaneously” should include the date they were created.

• The labels and stamps for the Exhibits should follow the lender’s exact instructions. Stamping an original document improperly may cause the original to be voided and a loan package can then be deemed incomplete.

5. Best Practices for Name Variations: Including Name Affidavit(s) stating all name variations is best practice, even when not required by the lender to close.

As bank attorneys for many lenders, loan processors, and closing departments, the above tips should serve as a general guideline only. Our office created specific bank teams dedicated to each lender we represent because the most important lesson we can impart is simply that each lender will have their own unique process and specific closing requirements. Taking care to review and understand the lender’s requirements prior to closing will make all the difference for that lender afterwards.

PLEASE NOTE: This article is intended for informational purposes only and does not constitute the dissemination of legal advice. The deadlines and some of the legal language discussed herein is subject to negotiation between the parties involved and/or interpretation by a court of law. We encourage you to speak with the attorney handling your specific transaction for further details.