Deadlines Within Deadlines: Cooperative Board Packages and Commitment Letters in NYC Real Estate Closings

A buyer (for purposes of this article, let’s call her Sally Streetwise) works with her broker to find a property she loves in a beautiful cooperative. The brokers work with the buyer and the seller to reach agreement on the key deal points and then turn the delicate deal over to the lawyers to conduct due diligence and to negotiate the more formal contract terms. After much back and forth between lawyers and clients, the contract is finalized, the buyer signs the contract and submits her deposit check, the seller’s attorney deposits the check to an escrow account, and the contract is fully executed.

You might think this would be a great point in time for the brokers, lawyers, buyers and sellers to take a collective sigh of relief, pat themselves on the backs, and look forward to a smooth closing. Alas, there is no rest for the weary in Manhattan real estate. With the finalization of the contract comes something lawyers and brokers deal with every day of their careers, but something first-time buyers like Sally Streetwise may not yet be fully prepared: DEADLINES, and the pitfalls for missing them.

The New York residential real estate contract will not satisfy itself with simply one deadline. There must be multiple deadlines, as many deadlines as there are subway lines (or double-parked cars) in Manhattan: Deadlines to apply for mortgages. Deadlines to obtain Commitment Letters. Deadlines to submit board packages. Deadlines for providing notices. Deadlines to schedule closings. Deadlines to adjourn closings. Deadlines that increase stress and confuse everyone throughout the process. While some lawyers, bankers, and brokers push forward as quickly as possible hoping that they avoid any deadline land mines, experienced practitioners will help the buyer navigate deadlines to lessen their stress and protect their best interests.

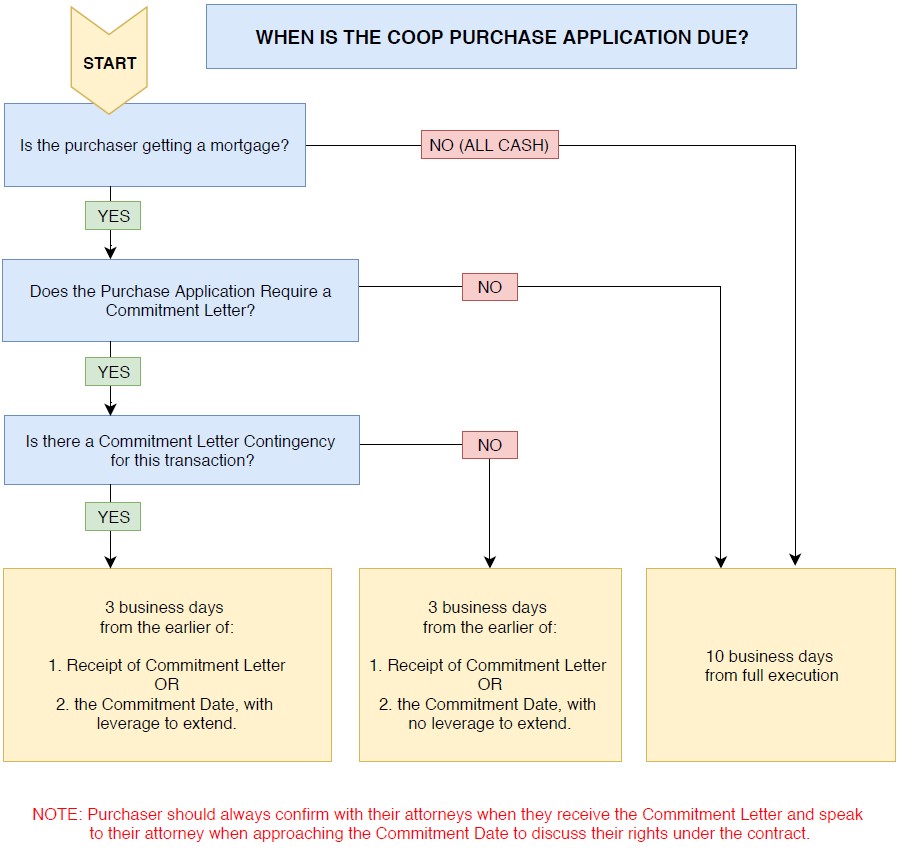

Let’s spend a few minutes to get acquainted with two of the most significant deadlines our buyer will encounter once she gets into contract: the board package submission deadline and the loan Commitment Letter deadline (“Commitment Date”). In the typical contract for the purchase of a cooperative unit, the answer is clear: Sally Streetwise has ten business days to submit her board package. Unless she has three business days. But remember that the three-business-day deadline begins to run at the expiration of a completely different thirty or forty-five-calendar-day Commitment Date. Sometimes. Or it begins to run sooner.

Let’s break that down a little bit further to clear up this confusion. One commonly used contract contains multiple deadlines for the submission of the board package, depending on different circumstances that might exist:

If Sally Streetwise is not seeking financing, and is proceeding “all cash,” she will need to submit her board package within ten business days of her attorney’s receipt of a fully executed contract (unless otherwise negotiated).

If Sally is seeking financing, then the determining factor for the board package deadline will be whether a commitment letter is required to be submitted with her board package. If the board does not require a commitment letter as part of the board package, then the original ten-business-day deadline is still in effect. However, most boards do require a commitment letter because most boards reasonably believe that if a buyer is unable to obtain a commitment letter, the deal will not go forward. There would be no point wasting time reviewing such an application.

If the board requires a commitment letter as part of the board package, then it’s important to note that the contract will include the Commitment Date of usually thirty or forty-five days from the date Sally’s attorney receives a fully executed contract. Sally’s board package deadline also then hinges on whether her contract has a Commitment Letter contingency.

If Sally’s contract has a Commitment Letter contingency, then her deadline is three business days from the earlier of when she receives the Commitment Letter or the Commitment Date.

If, on the other hand, Sally is seeking financing but her transaction does not include a Commitment Letter contingency, then Sally’s deadline is three business days from the earlier of: (1) when she receives the Commitment Letter or (2) the Commitment Date, with one important caveat: even if Sally has not obtained a Commitment Letter by the Commitment Date, she must still submit her board package within three business days from the Commitment Date.

Given the complexity described above, we would always recommend that a potential buyer, with the assistance of her broker, obtain a copy of the board application before entering into the contract for the purchase of the cooperative unit. This way they will know ahead of time whether the board requires the commitment letter as part of the board package and thus the deadline to submit that package. The broker and the buyer should work together to get the board package as complete as possible so that the only open item remaining while approaching the Commitment Date will be the lender’s issuance of a Commitment Letter.

One common pitfall to note: we all come across deadlines in our daily lives. When facing a deadline, there’s often an impulse to hurry up and beat the deadline by as many days as you can. In the context of the Commitment Date described above, and board package deadline, however, this is not necessarily the best path forward.

Once parties are in contract, Sally Streetwise should start working on her loan with her banker and on the board package with her broker. The goal for both is not necessarily to beat the deadlines to a pulp, but rather to meet the deadlines with the best work product possible within the time permitted.

For bankers working on the commitment letter, a number of open conditions may initially exist on the commitment letter and the banker should work with the client to try to eliminate as many open conditions as possible prior to the Commitment Date. For example, if a banker states that Sally Streetwise’s parents must provide a “gift letter” for funds that were given to her to purchase her first home, it would be best to obtain the gift letter and have that condition cleared from the commitment letter, rather than having the commitment letter issued with the open condition. What if Sally’s parents refuse to sign a “gift letter” for the funds they provided her? These types of potential issues would be better discovered while in the contingency period rather than after the contingency has lapsed.

It is also critical to have an experienced banker who is familiar with the interplay of the Commitment Date and the board package timeframes. Less experienced bankers may issue a commitment letter quickly in an apparent effort to impress the borrower, but inadvertently trigger the 3-day deadline described above when the borrower is not yet ready to submit the board package.

With respect to the board package, Sally Streetwise will want to have an open dialogue with both her banker and her broker, so that they take the time to prepare a board package that shows Sally in the best light and is most likely to result in board approval. Sometimes this means waiting until the most recent bank statements are available from the buyer’s bank, or waiting until the perfect source of a professional reference is back from vacation.

There is one notable exception to the above. What should Sally do when she obtains a commitment letter that is still subject to a satisfactory appraisal, but the appraisal has not yet been conducted or approved by the bank? In such a case, the typical real estate contract states that a commitment letter subject to an appraisal is not a “Commitment Letter” as defined in the contract unless and until the appraisal condition is satisfied. The first goal would be to make sure the appraisal is satisfied before sending the Commitment Letter as part of the board package. However, there are times that the broker will want to submit the board package quickly, for example to make the next board meeting deadline, and so they would prefer to submit the commitment letter with the appraisal condition. In such a case, the buyer may decide to submit the commitment letter even though it is still subject to an appraisal, but the buyer should state that it is a preliminary commitment letter with their right to cancel still intact under the standard commitment letter contingency clause.

One final note on deadline extensions: buyers should take note that in the world of contract law, there is a difference between a deadline where a buyer is given a right of action and a deadline where a buyer has no such right. For example, take the case where a buyer with a finance contingency has done her best to cooperate with the bank to obtain a commitment letter, but through no fault of her own, the bank is unable to issue the commitment letter prior to the typical thirty-day deadline. In such a case, the buyer would potentially have the right to cancel the contract. Given that right, there is a possibility that a buyer could request from the seller an extension of that deadline rather exercising the right of cancellation. This wielding of the implied power to cancel often results in the seller granting an extension.

Contrast this situation with the deadline to submit a board package. Here, in the normal circumstance, the buyer does not have a right to cancel if the board package is not submitted on time, and therefore may not be successful in seeking an extension of such a time. Seeking an extension in such a circumstance comes with risk. If the seller does not agree (and there is no requirement that they do) then the buyer must rush to submit the board package or risk being held in breach of the contract, which potentially subjects the buyer to the loss of the deposit. If a broker or client is concerned with the board package submission deadline, the most effective time to address this concern is during the contract negotiation stage, when additional time can be added to the contract.

Due to the complex interplay of deadlines described herein, it is imperative that a buyer work with seasoned professionals when selecting a lawyer, broker, and banker. Each of these professionals works with the others to ensure that the deadlines are effectively met and with information that puts the buyer in the best possible position to succeed in the transaction.

PLEASE NOTE: This article is intended for informational purposes only and does not constitute the dissemination of legal advice. The deadlines and some of the legal language discussed herein is subject to negotiation between the parties involved and/or interpretation by a court of law. We encourage you to speak with the attorney handling your specific transaction for further details.

Cutting Through the Smoke: Applying Local Laws 141 & 147 to Cooperatives and Condominiums in New York City

As public opinion has turned against smoking, NY laws have followed. Smoking bans in public spaces have included stores, schools, and taxis in 1990, bans in restaurants and indoor bars in 2002, and parks, beaches, and pedestrian plazas in 2011. The popularity of the smoking bans in our public spaces have let legislative sights turn to residential buildings. The latest is Local Law 147 (“LL147”). Effective on August 28, 2018, LL147 requires residential buildings with three or more units to develop and distribute a written smoking policy. However, unlike the smoking bans, LL147 does not require condominium or cooperative boards to ban smoking in its entirety. Instead, it forces boards and unit owners to have a hard conversation and clarify what neighbors expect of each other. On its face, LL147 is agnostic about the content of the new smoking policies; it only asks that clear building policies are being put in place.

Even the laxest smoking policies distributed under LL147 may still be subject to other smoking laws targeting residential buildings, like Local Law 141 (“LL141”) which prohibits smoking or using electronic cigarettes in the common areas of most residential buildings. LL147 can make LL141 more transparent for residents by clearly outlining a smoking prohibition in the shared common areas while clarifying how the building will treat limited common elements like personal balconies and any other outdoor areas that may be connected to residential units.

On the other hand, for buildings looking to adopt a stricter policy, LL147 leaves open the door for boards to discuss and mandate a completely smoke-free environment throughout the building – including within individual apartments. If a board decides to go completely smoke-free, and adopts a new policy using the proper governing mechanisms, all residents may be required to follow the policy, including unit owners, their future renters (current renters may be carved out depending on their leases), and anyone invited onto the premises. Because LL147 leaves it to the buildings to self-govern, it sidesteps the issue of whether the law allows for strict regulations that pierce the sanctity of the home. Even buildings whose residents largely support going smoke-free may still be cautious about how a strict ban can be properly applied, implemented, and enforced.

Like pet policies, smoking policies can feel very personal. For prospective purchasers sensitive to smoke or those who are avid smokers, reviewing the new smoking policy is another important item to flag for your brokers and attorneys during the diligence phase of vetting a new home. But for unit owners caught off guard by a new strict policy or prospective buyers who don’t like what the diligence reveals, know that ultimately any policy is subject to change; it comes down to what your board and your neighbors want. Ultimately LL147 is just a harbinger – potentially showing a trend towards stricter smoking regulations to come.

5 Things to Consider When Choosing a NYC Real Estate Attorney

When buying or selling a property, a knowledgeable lawyer that practices Real Estate law will help make sure you get exactly what you want out of the transaction.

1. Knowledge of New York City Residential Transactions

The “Concrete Jungle” has a unique housing stock unlike anywhere else in the U.S. For example, the great majority of Co-ops that exist in the U.S. are in New York City. Because of these unique features, there are intricacies to closing a NYC Real Estate Transaction that a well-qualified attorney can help to explain. These include things like knowledge of local regulations, understanding the custom and practices in cooperative, condominium and house purchases, experience dealing with the New York City network of brokers. Additionally, it is preferable to have an attorney who has completed sales in the building, or similar buildings, that you plan to buy/sell in. Knowledge in the field means knowing what to look for to ensure the transaction goes as smoothly as possible.

2. Personalized Attention

You do not want a Real Estate Attorney who takes a cookie cutter approach to one of the most important transactions of your life. A good real estate attorney will give you personalized attention and be available to answer the questions you have when they come up. To achieve this, it is important to have a team of individuals working on your transaction, rather than just one person. Extra sets of eyes ensure that details are not overlooked.

Also, you want to make sure that an attorney is working on your transaction, not just a paralegal or an administrative assistant. Some firms assign only a paralegal to the transaction, a practice we do not employ. Many times we have two attorneys working on one transaction, both for a smooth client experience and to allocate resources where they are most needed.

Like a doctor with good bedside manner, a good attorney will form a close bond with their client that is based on mutual respect and trust. Despite all the lawyer jokes you may have heard, most attorneys are hard-working, excellence driven, respectful individuals who are trying to do their best for their clients. Our firm puts a focus on this aspect of the relationship because we feel it is the centerpiece of the real estate transaction puzzle.

3. Fees

Fees will vary depending on the size and complexity of a transaction. They will generally be structured as a flat fee, with half payable up front and the balance payable after closing. Factors that affect the fee, include but are not limited to: (1) whether the purchase will be made in cash or require a mortgage; (2) if there is a lender, whether it is an institutional or a private lender; (3) whether the transaction involves Federal or State tax withholdings; (4) whether the client will be able to attend the closing; (5) whether there are any anticipated title issues; (6) whether the transaction includes anything that is not part of the normal process of buying or selling a property in NYC.

Some firms will refer to all or a portion of the fee as “non-refundable.” We do not agree with this approach and will refund any unused portion of the retainer on any transaction. Other firms will say “no fee if we do not get you to the closing.” We do not agree with this approach either, as we feel it will create a conflict of interest where the attorney may unconsciously rush to conclude a transaction or hold back emphasis on any issues that arise that might jeopardize the transaction in any way.

See an article on the firm’s origin and philosophy here.

4. Provide Consultation and Guidance on all Aspects of the Transactions

A good real estate attorney will advise you on all of the risks associated with the transaction and guide you on how to proceed. They will advise you, not only on the legal aspects of the transaction, but also help you to identify and manage the wide assortment of risks that affect the viability of a residential transaction. This includes reviewing board minutes, building financials, the offering plan, and other important documents. In addition, an attorney will help you coordinate a loan commitment, negotiate a contract for a sale and much more.

A good attorney will also know how to allow a client to be a valuable resource as well. Even if a client knows nothing about real estate or financing, they can still provide key information about the condition of the property, what it looks like, what they expect to receive, and what their most important needs are from the property. A good attorney will know when to ask questions and when to provide answers, while a not-so-good attorney thinks they know all the answers and never asks a single question.

5. Team Player with Proven Track Record

It is important to choose an attorney who is empathetic to your needs, works well with others, and has a proven track record supported by professional referrals. Ultimately, choosing an attorney is a very personal process. Check out information on our firm here!

NYC Real Estate Attorney’s Closing Report: June 2018

Just a few of our recent closings. If you are also looking to buy or sell at these property addresses, you might want to give us a call.

| Property | Value | Transaction |

| 1060 Park Avenue, NY, NY | $1,317,500 | Coop Purchase |

| 300 West 135th Street, NY, NY | $1,040,000 | Condo Purchase |

| 420 East 51st Street, NY, NY | $645,000 | Coop Sale |

| 401 East 86th Street, NY, NY | $1,349,000 | Coop Purchase |

| 525 East 86th Street, NY, NY | $825,000 | Coop Sale |

| 170 John Street, NY, NY | $2,300,000 | Condo Sale |

| 132 East 35th Street, NY, NY | $865,000 | Coop Sale |

| 561 41st Street, BK, NY | $582,500 | Coop Purchase |

| 680 West 204th Street, NY, NY | $380,000 | Coop Purchase |

| 1199 Park Avenue, NY, NY | $3,325,000 | Coop Purchase |

A Guide to the Tax Law With Marjorie Dybec

If you have been wondering how the new Tax Law will affect your real estate taxes, please take a moment to watch this helpful video prepared by broker Marjorie Dybec of Douglas Elliman Real Estate.

NYC Real Estate Attorney’s Closing Report: May 2018

Just a few of our recent closings. If you are also looking to buy or sell at these property addresses, you might want to give us a call.

| Property | Value | Transaction |

| 68 Hart Street, BK, NY | $1,500,000 | House Purchase |

| 888 Fulton Street, BK, NY | $849,388.00 | Condo Sale |

| 504 West 111th Street, NY, NY | $725,000 | Condo Purchase |

| 762 Park Place, BK, NY | $795,000 | Condo Purchase |

| 13 West 13th Street, NY, NY | $590,000 | Coop Purchase |

| 88 Wyckoff Street, BK, NY | $1,010,000 | Condo Sale |

| 549 East 11th Street, NY, NY | $1,550,000 | Condo Purchase |

| 17 East 17th Street, BK, NY | $595,000 | Condo Purchase |

| 250 West 22nd Street, NY, NY | $930,000 | Coop Purchase |

| 30 East 10th Street, NY, NY | $2,625,000 | Coop Purchase |

WHFirm Attorney Hosts Due Diligence Lecture

Congratulations to WHFirm Junior Partner Michael Zadjelovich, who recently hosted a “lunch and learn” at Halstead Realty in Brooklyn. The lecture, aimed at educating brokers about the process of Due Diligence, was both well-attended and well-received.

Thanks also to Halstead Realty for making this event possible, and of course to all of our attendees!